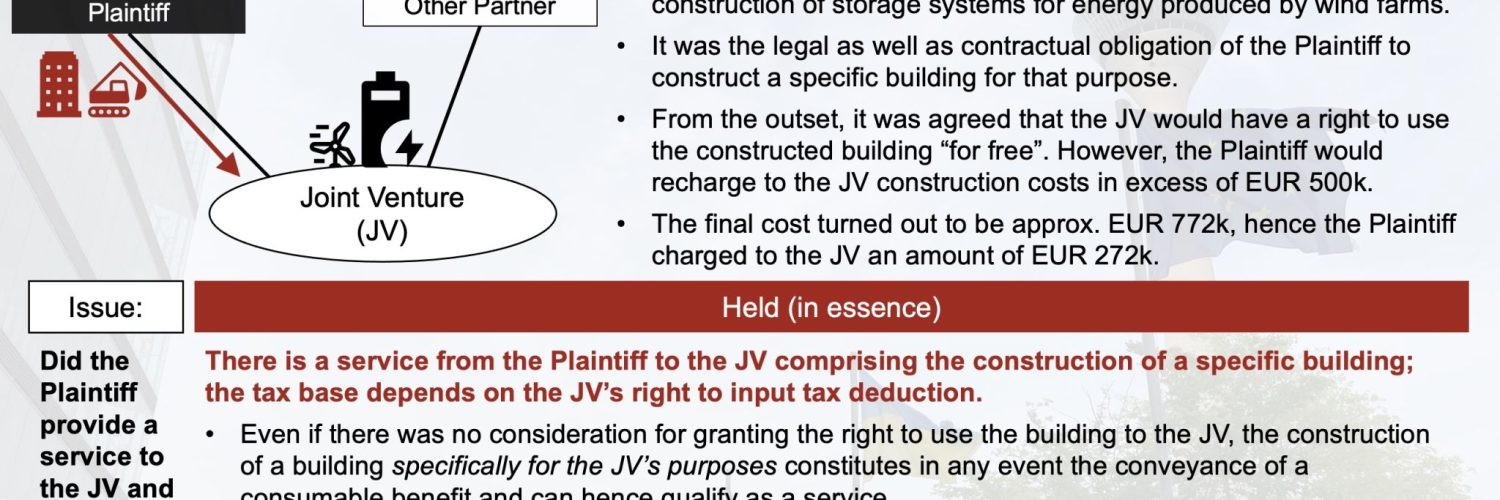

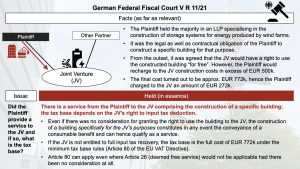

The case involved a taxpayer constructing a building for another party and allowing them to use it for free. The State Court initially ruled that there was no supply because the user did not receive anything in return for the construction costs. However, the Federal Court disagreed, stating that the construction of the building could be classified as a service and that the tax base could be elevated to EUR 772 due to some consideration being present. The interplay between Articles 26 and 80 of VAT law was noted as creating anomalous results, which the CJEU may need to review.

Source Fabian Barth