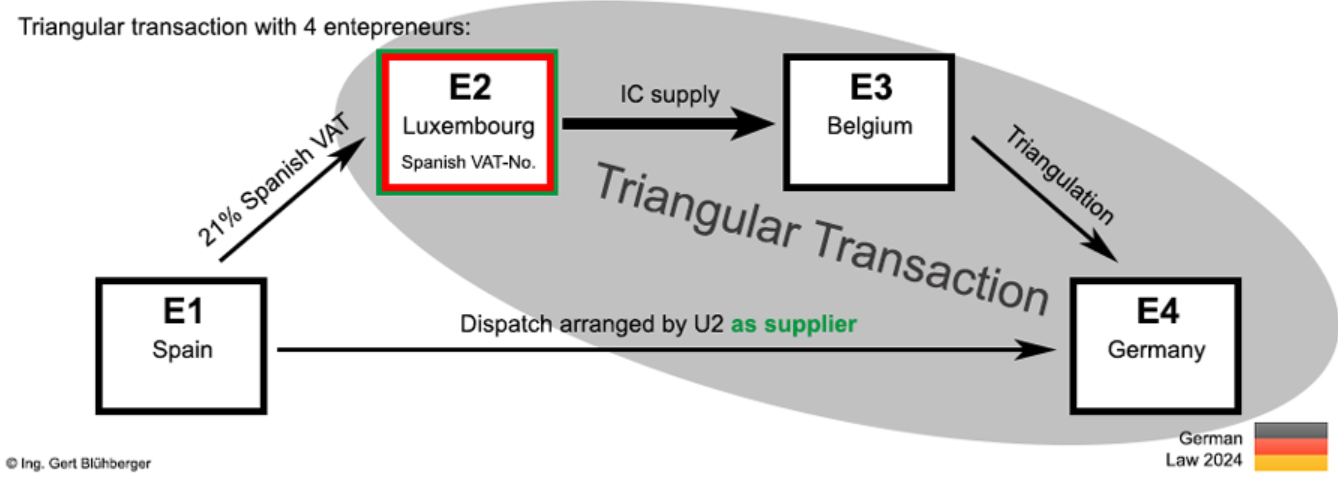

- Community Triangular Transactions: Involve goods sold across three EU member states. Here, the goods move directly from Germany to Austria, bypassing France, which affects VAT handling.

- Solution 1 – Physical Flow Principle: The French company (B) must obtain an Austrian VAT number, as the goods physically move from Germany to Austria. The German company invoices without VAT, and the French company reverse charges Austrian VAT. The final invoice from France to Austria includes Austrian VAT.

- Solution 2 – Simplification via Directive 2006/112/EC: Avoids the need for the French company to register for Austrian VAT. The German company invoices without VAT, using the French VAT number of company B. The French company annotates the invoice with Directive 2006/112/EC and uses a “reverse charge by the lessee” note for the Austrian customer.

- VAT Returns and Declarations: For Solution 1, the French company files Austrian VAT returns. For Solution 2, the transaction is declared in French VAT returns (line E2 CA3) and specific statistical declarations, with Austria as the destination.

- Austrian Customer’s Role: In both solutions, the Austrian company self-liquidates VAT, deducting it on its Austrian VAT return.

Source Legifiscal

Latest Posts in "European Union"

- ViDA – Transfer of Own Goods Scheme and its Intrastat Implications

- Roadtrip through ECJ Cases – Focus on ”Public bodies” (Art. 13)

- Latest Trends in Global VAT Compliance for Online Businesses in 2026

- EU – IOSS Scheme: Customs & Business Benefits for E-Commerce Vendors

- Comments on ECJ C-527/24: Right to VAT Refund Despite Technical Glitch in Cross-Border Application